KEY MESSAGES:

- Findings support the phenomenon known as the “retirement savings crisis”. Many researches have shown that people are at risk of entering retirement without the resources necessary to maintain their standard of living and provide the financial security they need for their retirement years.

- Survey findings highlight serious concerns about the ability of financial advisors to provide unbiased, professional advice as only 37% of respondents agreed that financial advisors are in general reliable.

- When it comes to mode of communication with their financial advisors, majority of respondents are conservative with 66% prefer face-to-face interactions.

- Survey results also indicate that investors are not interested in a “digital-only” relationship. Undoubtedly, technology is the way forward for wealth managers in a competitive financial landscape. But communication should not be limited to virtual channels, and digitisation should not be seen as a replacement for the bonds of trust formed by human relationships.

Cambridge IF Analytica conducted a study titled “Demystifying Islamic Wealth Management: Consumer’s Knowledge and Preferences”. This study aimed to assess consumers’ knowledge levels on Islamic wealth management products and identify factors that affect their choice of Islamic wealth management products and services.

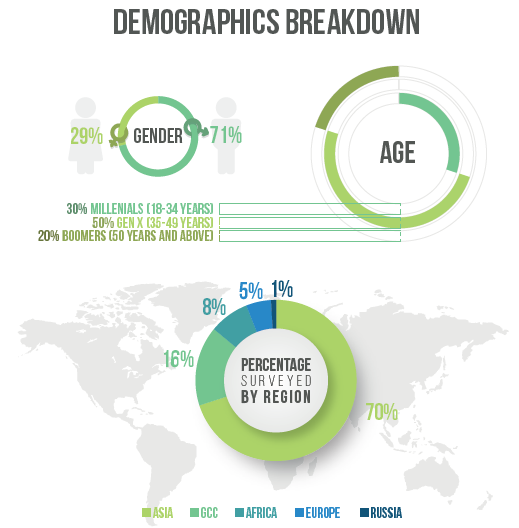

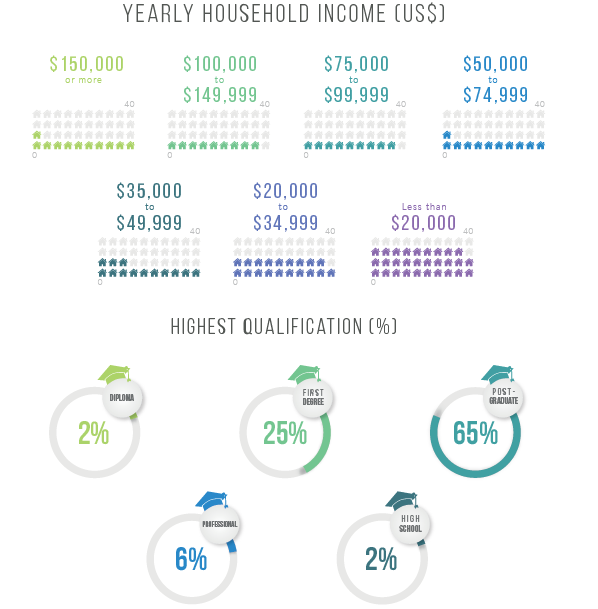

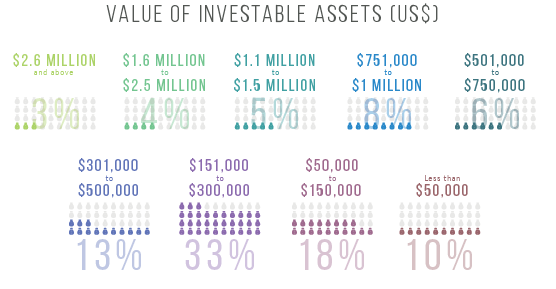

We surveyed 806 individuals in 26 countries spanning across 5 continents to help wealth management firms understand consumers’ knowledge, attitudes and behaviours. Respondents were consumers of Islamic banking, takaful and Islamic wealth management services. Our survey respondents were predominantly in their mid-30s to early 40s, well-educated and have investable assets ranging from US$151,000 to US$500,000.

Financial Priorities & Knowledge

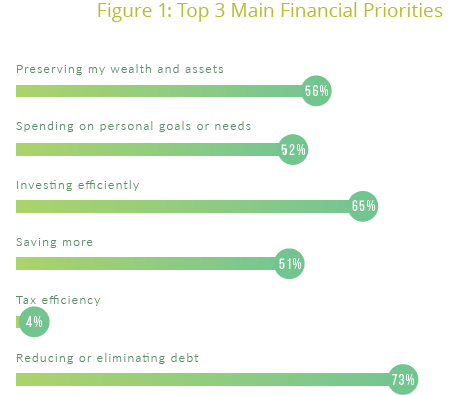

In these uncertain economic times, having a financial cushion is a priority for many. When asked to rank the importance of various financial priorities, reducing or eliminating debt was the overwhelming first choice (73%) as shown in Figure 1. This is followed by investmment efficiency (65%), preserving wealth and assets (56%), spending on personal goals and needs (52%) and to save more (51%). However, overall tax efficiency is the lowest priority with only 4% of surveyed respondents cited this as their financial priority. This offers some interesting insights into where consumers stand with their finances. Clearly, respondents prioritised debt reduction and investments over savings. It should be noted here that financial priorities will depend on what stage of life a person is at. For example, a young professional will focus more on building up a deposit to buy a house. Whilst an older person will be planning for retirement.

The study shows that the younger generations have different priorities than their older cohorts. One crucial area where this is evident is wealth preservation. Six in ten Boomers in this survey (60%) have preserving wealth and assets as their number one financial priority, and nearly half (49%) of Gen X or Millenials are focused on investing their money efficiently. It is perhaps not surprising that 88% of Millennials cited saving more as their top financial priority.

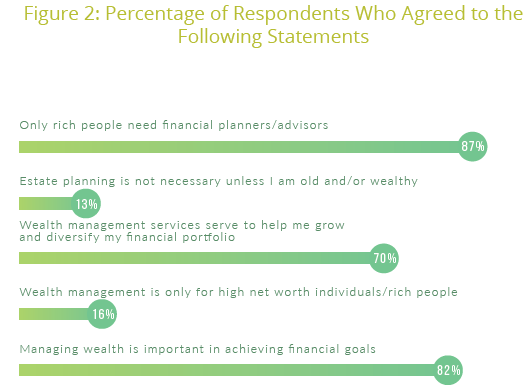

87% of surveyed respondents believed that only rich people need financial advisors. Part of this misconception may be rooted in the fact that people often lump financial advisers in the same category as other financial service providers such as lawyers who often charge expensive retainers. In many cases, price is one of the biggest factors discouraging people from seeking help from financial professionals or experts.

Another interesting finding is that about 83% of the respondents viewed estate planning as only meant for the rich or old people. While this view is common amongst the majority of respondents surveyed, it couldn’t be further from the truth. In fact, proper estate planning can help people across the wealth spectrum to achieve numerous goals. However, about 82% agreed that managing wealth is important in achieving their financial goals. Meanwhile seven in ten respondents are of the view that wealth management services serve to help them grow and diversify their financial portfolio.

Keeping a Finger on the Pulse of Islamic Wealth Management

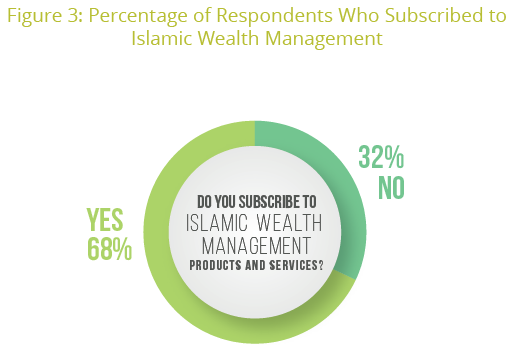

Respondents were asked if they had subscribed to any Islamic wealth management products or services. As shown in Figure 3, 68% said they do. Of these 20% subscribed to both conventional and Islamic wealth management products and services.

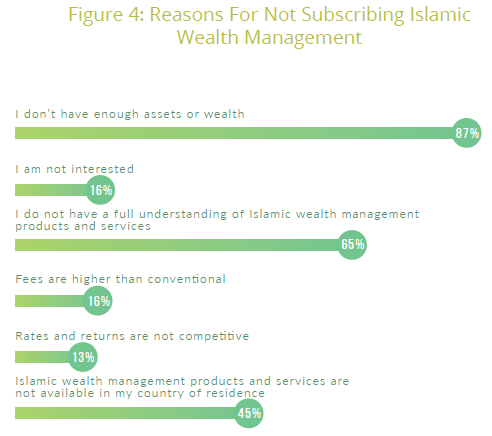

But 32% do not own any Islamic wealth management products. The reason? 87% of them cited not having enough assets as the primary reason (Figure 4). Nearly two-thirds of respondents expressed lack of understanding of Islamic wealth management, suggesting that lack of knowledge is a barrier to the growth of the industry. Another 45% said they are not able to subscribe to Islamic wealth management products and services because these are not available in their country of residence, implying a huge untapped opportunity for the Islamic wealth management industry.

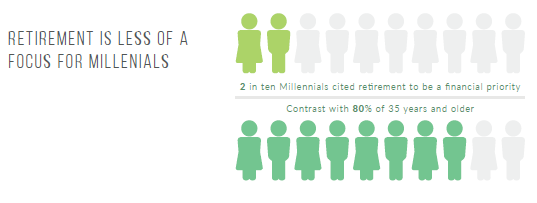

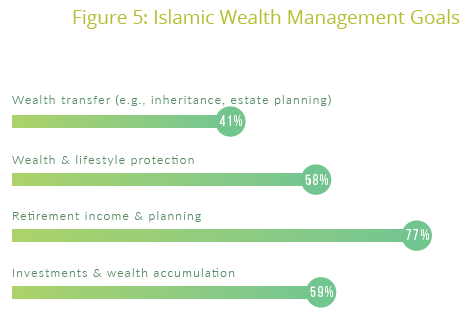

When it comes to Islamic wealth management goals, majority (77%) surveyed cited retirement income and planning as their primary goal (Figure 5). This is followed by investments and wealth accumulation (59%) and wealth and lifestyle protection (58%). This reflects the growing awareness about long-term financial planning, including for retirement. For most people, planning a comfortable retirement can’t be done in a matter of a couple years — it takes decades of diligent planning and savings to reach retirement goals. Gen Xers and Boomers, who see retirement on the horizon, are by far the most focused with this goal in mind, where 80% of them cited retirement to be a financial priority. This is a stark contrast to only 20% of Millennials.

Our findings also support the phenomenon known as the “retirement savings crisis” and consistent with the earlier findings on financial priorities of respondents. Many researches have shown that people are at risk of entering retirement without the resources necessary to maintain their standard of living and provide the financial security they need for their retirement years. Factors such as sustained rises in health care costs, increased life expectancy and the possibility of future reductions in government-provided retirement benefits have contributed to the “retirement savings crisis”. All of these contribute to a greater need for financial advising that goes well beyond investment advice.

These Islamic wealth management goals far outranked wealth transfer where less than half of respondents (41%) stated wealth transfer as a goal. Clearly, consumers placed greater priority on income production than to preserve and plan for transference of wealth to progeny in a Shari’a-com-pliant manner, which is an important goal of Islamic wealth management. Although wealth distribution among heirs is determined by Islamic inheritance law, the need for estate planning is vital as it offers financial sustainability and great satisfaction to its entitled beneficiaries. This is particularly true in countries where Islamic inheritance law doesn’t have a role in the judicial system. Factors such as low level of awareness of Islamic estate planning and the misconception that estate planning only applies to wealthy individuals with millions in assets explain why estate planning amongst Muslims is not widely practiced. Chapter 4 offers a comprehensive discussion on Islamic estate planning.

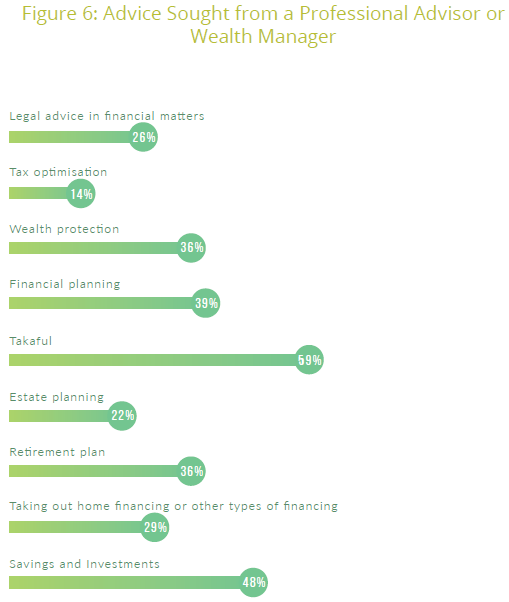

Despite retirement income and planning was the primary Islamic wealth management goal of more than 70% of respondents, only 36% had sought any advice on retirement plan from a professional financial advisor or wealth manager (Figure 6). Majority sought advice on takaful products (59%) and savings and investments products (48%). An alarming finding is that only 39% of surveyed respondents said they had consulted a professional advisor on financial planning. But to have a better understanding of barriers to financial advice, one must examine seeking of advice by consumers and delivery of advice by professional financial advisors.

The study also pinpointed profound gender differences in financial planning attitudes and practices. While 90% of women who took part in this survey sought and used financial advisors, only 67% of men did so. Hence, the study supports evidence that women are more likely to seek and actually use financial advisors, while men are more likely to get information on their own. Various studies have shown that men are less likely to pursue financial advice because of their overconfidence in their own abilities and preference for self-directed learning. While each person is shaped by his or her own individual experiences, there is some compelling research on gender and finance that raises potential barriers to advices seeking by both men and women.

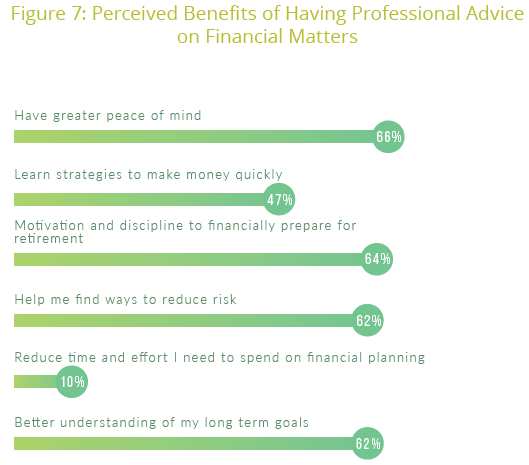

When asked to rank the benefits of having professional advice, nearly two-thirds of respondents revealed that ‘having greater peace of mind’, ‘motivations and discipline to financially prepare for retirement’ and ‘help find ways to reduce risk and better understanding long term goals’ were their top four benefits (Figure 7). 47% of respondents think that engaging professional advice would help them learn strategies to make money quickly. The results show quite clearly that it is not just about getting a decent return on money, but it’s having a plan in place to deal with economic uncertainties and help keep you on track to achieving your goals.

However, only 10% of respondents thought that a major benefit of a financial advisor or planner would be that they would spend less time and effort on financial planning. The results have serious implications for the Islamic wealth management industry in general, and Islamic financial planning in particular. Although they perceive many benefits from receiving profes-sional financial advice, consumers are sceptical of the financial advice received and are less likely to view financial advisors as trusted sources.

Appetite for Expertise

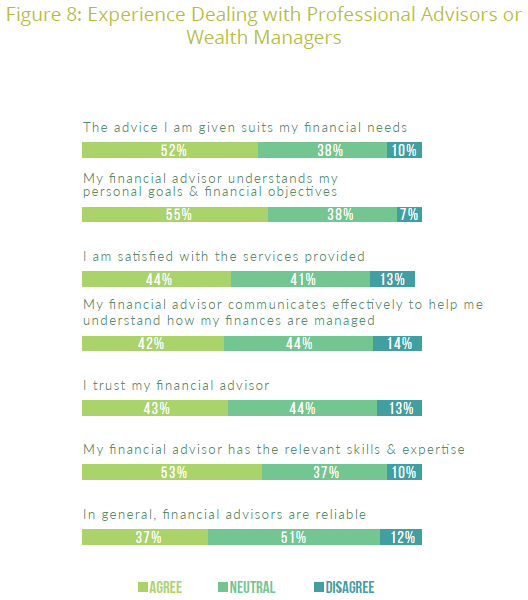

In describing their experience with financial advisors, majority of those who used a financial planner or wealth manager said that their financial advisors understood their personal goals and financial objectives (55%) and have the relevant skills and expertise (53%), whilst 52% said that the advice suited their financial needs (Figure 8). Less than half of the respondents were satisfied with the services provided (44%) and trusted their financial advisors (43%).

Only 42% thought that their financial advisors had communicated effectively on how their finances are managed. The findings highlight serious concerns about the ability of financial advisors to provide unbiased, professional advice as only 37% of respondents agreed that financial advisors are in general reliable.

The level of distrust is alarming for financial institutions and agencies/associations and is consistent with the populous view of the industry post the financial crisis, which had led to a distrust of financial advisors. This raises the issue of whether financial advisors show a satisfactory level of professionalism and ethics towards their clients. It is therefore vital for financial institutions to use effective communication and marketing strategies such as using social media and blogs to mitigate this lack of trust.

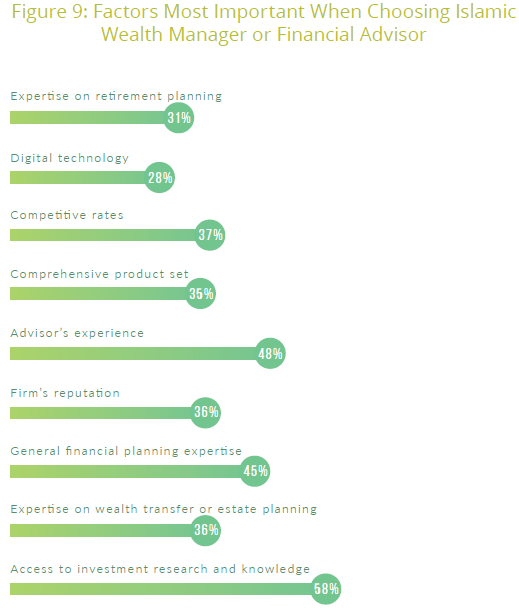

By far the most important reason for choosing Islamic wealth managers or financial advisors cited by the surveyed respondents is access to investment expertise (58%) (Figure 9). The second reason is their years of practical experience (48%), followed by their expertise in general financial planning (45%). These factors far outweigh firm’s reputation (36%) and competitive rates (37%). Hence, implying that respondents are willing to pay for the services provided because they are looking for an advisor with the expertise to help them navigate the complexities of the financial markets.

Personal Interactions are Preferred with Digital Channels Playing Complementary Role

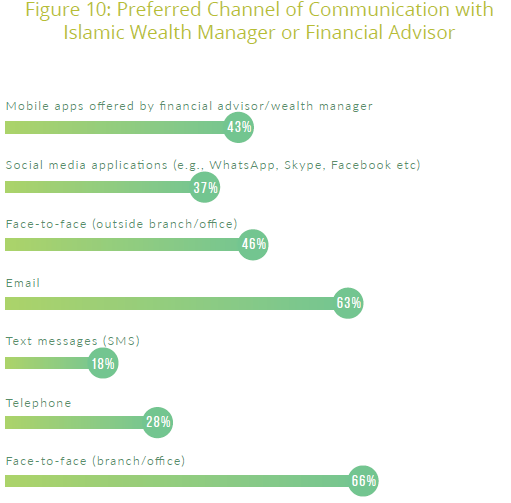

When it comes to mode of communication with their financial advisors, majority of respondents are conservative with 66% preferred face-to-face interactions at the office or branch (Figure 10). Another 63% of respondents cited email as their preferred channel of communication. Investors’ perceived importance of these interactions reveal strong preferences for personal interaction, as well as other traditional channels. Survey results also indicate that investors are not interested in a “digital-only” relationship. Undoubtedly, technology is the way forward for wealth managers in a competitive financial landscape. But communication should not be limited to virtual channels, and digitisation should not be seen as a replacement for the bonds of trust formed by human relationships.

What is interesting here is that only 37% would like to communicate via social media applications, implying that traditional channels continue to be the primary medium for interaction with an advisor, including discussing finances or obtaining information. Although digital channels play a complementary role, more than 43% of surveyed respondents preferred mobile apps as opposed to social media (37%). This relatively low appetite for using social media to communicate on financial matters is a reflection of consumers’ preference to keep their financial activities separate from their social networks.

Trust is a Barrier to Financial Advice

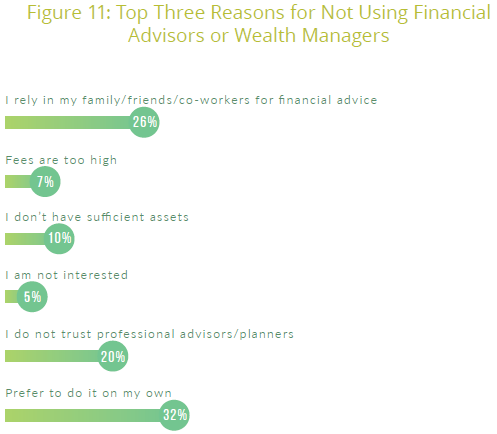

24% of respondents said they have never sought any advice from any financial advisors or wealth managers. Of these 88% were male, 71% had a postgraduate degree and 38% were between 18 and 30 years old. ‘Prefer to do it on my own’, ‘rely on family, friends and co-workers for financial advice’ and ‘do not trust professional advisors’ were the top 3 reasons for not using the professional financial advisory services (Figure 11). The results point to the fact that these people are sceptical about the value of financial advice, because they feel they have the ability to find financial information themselves.

Twenty-six percent of respondents who haven’t worked with a professional financial advisor say they have not done so because they prefer to seek advice from family, friends and co-workers. Although it is encouraging that financial matters are being discussed with family and friends, it is however prudent to handle some situations with the help of a competent professional advisor. Since professional financial advisors have broad experience working with many different clients and situations, they can quickly assess client’s need and offer sound advice that is tailored to their circumstances.

Trust is also a barrier to financial advice. The recent turmoil in the financial markets has significantly lowered consumers‘ confidence and trust in the financial services profession. Lack of trust is holding most consumers back from working with a financial professional, with 20% saying they did not trust professional advisors and planners. Hence, they are more likely to turn to family and friends for advice on financial planning matters or rely on websites and other sources for financial information. While informal advice may be customized to an individual household’s financial details, friends and family may be uninformed and therefore may provide inappropriate advice. However, given the current economic climate, it makes it even more important that people have access to affordable financial planning advice. The industry also needs to work together to change the idea that planning is only for the wealthy.

Digital is Key to Financial Management

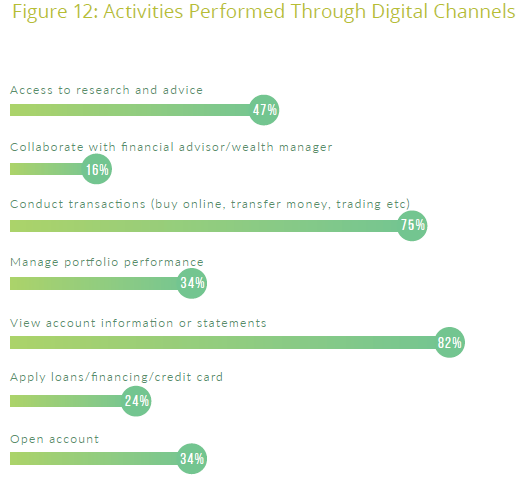

The study also analysed the activities conducted through digital channels, the digital interactions investors want, and their propensity to adopt digital offerings and use robo-advisors. Digital technology is already employed across a wide array of their financial and wealth management needs. As can be seen in Figure 12, majority of the transactions conducted through digital channels are basic banking transactions – view account or statement (82%) and conduct online transactions such as online purchase and money transfer (75%). Only a third were using online services for portfolio management.

About 47% of those surveyed used digital channels to access research and seek out advice on financial matters, thus seeking to become more educated about investing. The finding reveals an opportunity for wealth managers and financial advisors to provide relevant resources for investment education that can potentially help build trust. This could be the key to greater investor engagement.

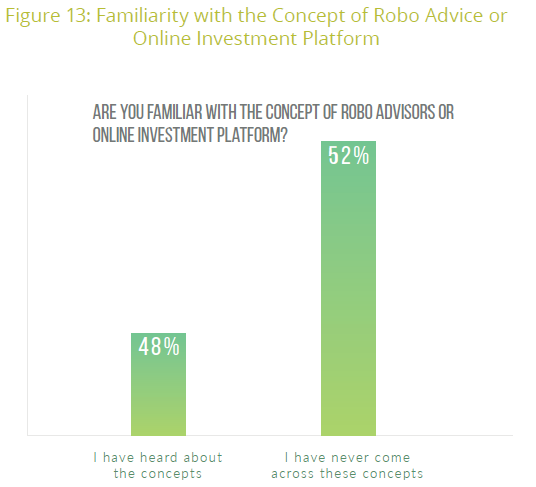

Nearly half (48%) of the surveyed respondents said they were familiar with the concept of robo advice (Figure 13). It should come as no surprise that familiarity and comfort levels with robo-advisors decrease with increasing age. Only 12% of Boomers were familiar with robo-advisors. The numbers change to 33% and 57% with Gen X and Millenials, respectively, which implies that there is a large market for automated financial advice.

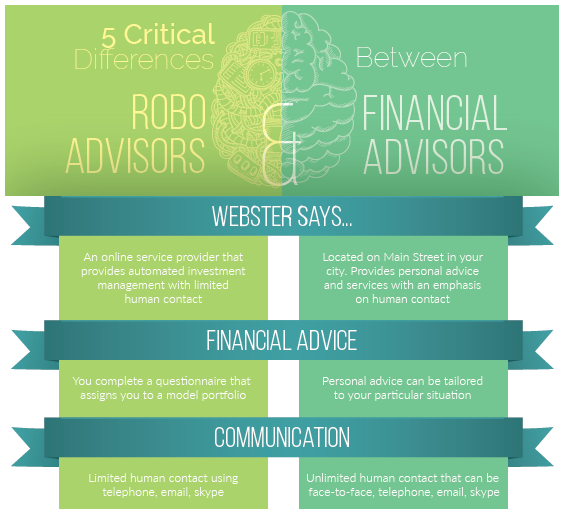

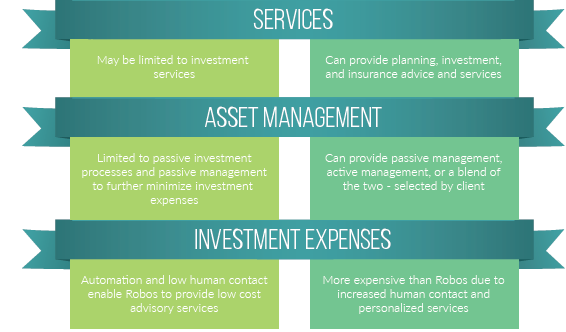

Robo advisor or also known as automated investing or online advisors, use computer algorithms and advanced softwares to build and manage a client’s investment portfolios, offering such features as automatic rebalancing and tax optimisation. Most robos have little or no investment minimums, so one does not have to be mega-rich to benefit from their advice. In addition, robo-advisors offer convenience and expertise for a fraction of the cost of a financial advisor.

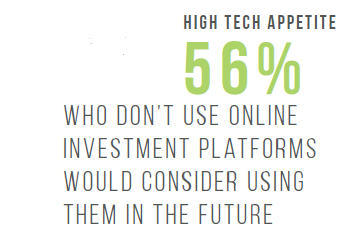

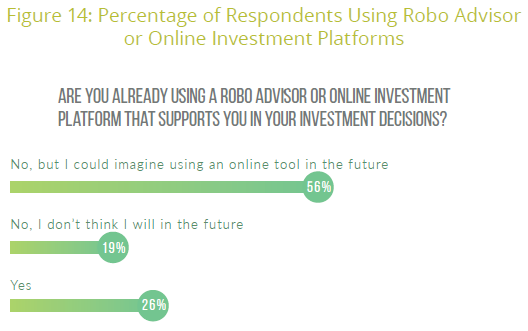

In the earlier sections, we reported that personal interaction was cited as the most preferred channel of communication with advisors. Hence, human touch is still required. But investors are increasingly aware of how automated technology can help them in making better and informed investment decisions. Of those who said they have heard of robo-advisors, over a quarter are actually using it whilst 56% said they haven’t explored robo-advisor services but could imagine using it in the future (Figure 14).

Our findings suggest that the future of investment advice lies at the intersection of technology and humanity.

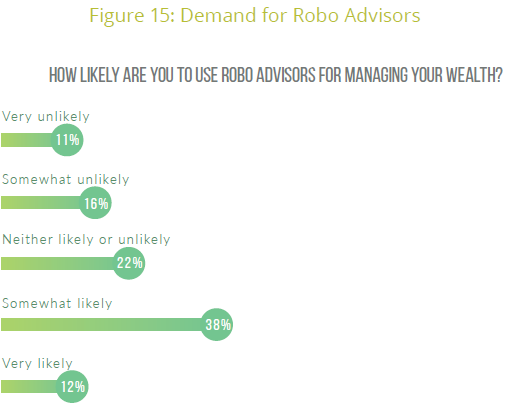

Of those respondents who are not using robo advisors, five in ten said they are likely to use these services for wealth management whilst 36% said they don’t think they will (Figure 15). With majority of the respondents positive to the adoption of an automated solution in Islamic wealth management, the future of financial advice will be digital.

{kind=link}