While unbanked population comprises around 25% of the world’s population, half of the global poverty resides in the Muslim world. Most of the Muslim population is also unbanked. Without the lower-income group having access to financing and basic financial services, reducing poverty in less-developed Muslim countries will be difficult. This highlights the need for FinTech solutions in improving financial inclusion. Therefore, it is not surprising to see innovations such as crowdfunding, e-money and advanced digital payment methods, blockchain, open banking, big data analysis and artificial intelligence are receiving increasing attention from regulators around the globe. Furthermore, these technologies have a multi-dimensional impact on societies where the new applications are spreading in every field including social and Islamic finance. This chapter investigates three FinTech areas, namely, crowdfunding, e-money and blockchain, and analyses how these advanced technologies could strengthen IsSF and enable it to achieve its goals. We will analyze the current development by analyzing the ongoing projects and exploring the most recent initiatives. Driven by the importance of blockchain, the chapter puts emphasis on blockchain applications on various areas including charities, zakat, waqf, microfinance and halal food industry.

Crowdfunding and P2P Financing

Crowdfunding platforms provide funding for projects, online by large number of people with small contributions. The idea is not new, but the widespread usage of internet and digital payments have made it popular in the last 10 years. Through specifically designed website platforms, socially beneficial projects are announced and marketed to be financed by the mass population in which funds are collected online through the same platform itself or through other specialized platforms.

Fundraising through crowdfunding platforms are usually offered in form of donations or loans with or without interest. However, in the last few years, equity crowdfunding started to get more attention. Hardly in practice before 2010, it is a source of funding to hundreds today. Through web-based platforms, project owners and developers can reach the potential investors, advertise their projects and demonstrate important information such as the investment goals and expected rate of returns with much lower cost as compared to the traditional pitching methods. Of course, the success of these platforms depends on their ability in providing transparent and credible information about the projects. Therefore, some crowdfunding investment platforms choose to provide oversight and governance mechanisms by evaluating the projects presented and offering other third-party risk assessment and rating services. Furthermore, some of these platforms became more like social networking websites that allow public to share activities, photos, etc.

There are no accurate data on the size and number of crowdfunding platforms today. While some reports estimate total size of around US$300 billion, a recent report from Cambridge Centre for Alternative Finance indicates that the total worldwide crowdfunding including Peer-to-peer lending and donations reached US$417 billion in 2017 up from US$289 billion in 2016 (CCAF, 2019 as cited by P2Pmarketdata, 2019). The latest data available on P2PMarketData confirmed also the rapid growth in all regions of the world with a worldwide growth rate of 44.2%. Though the market is largely dominated by US and China with more than 90%, Muslim countries are catching up recently. For instance, crowdfunding and P2P lending in Indonesia reached US$5.3 billion in November 2019 from less than US$1.7 billion in December 2018 (OJK, 2019). It is believed that a significant percentage of this P2P lending are for charities and socially beneficial projects including energy projects, affordable housing, microfinancing, and empowering women and young entrepreneurs projects. With such unprecedented high growth rates in Muslim countries, there is great potential for Islamic crowdfunding to grow.

THERE IS GREAT POTENTIAL FOR ISLAMIC CROWDFUNDING TO GROW

Among the well-known Islamic crowdfunding platforms is Ethis Ventures. It owns and partners with several crowdfunding platforms for several purposes. This includes waqf (endowment) and sadaqa (alms) platforms (waqfworld.org, yemenaid.com and muslimwomentech.com), Real Estate crowdfunding (EthisCrowd.com) and SME development (Kapitalboost.com). Furthermore, in 2016, Ethis Kapital (one of Ethis joint ventures) has been awarded with the first Shari’a-compliant P2P licence from Securities Commission Malaysia. While it is yet to see the results of Ethis Kapital investments in Malaysian market, Ethis Crowd reported that more than 8,300 affordable houses are financed and built in Indonesia with the help of the platform. Ethis Crowd chose to facilitate investments from around the world to finance affordable housing in Indonesia where a large portion of the low-income Muslims works informally, and hence, financially excluded. In fact, affordable housing is not a problem of developing countries only, low-income people in developed countries are also often forced to rent houses or to spend a huge portion of their income to service their housing loans, if they succeed to get one. According to UN, 35% of the world’s rural population lives in unacceptable conditions. Overall more than 2 billion people are in desperate need of better housing. This means that affordable housing is a very pressing challenge for all countries. Crowdfunding could be one of the solutions, especially if it is accompanied with sound regulation and good government support. For instance, the regulatory framework and governmental support including subsidising the affordable housing projects in Indonesia have created an incentive to the developers and created a market for social crowdfunding whereby small investors can earn decent returns while also contributing to a good cause.

A recent boost to the sector came with the involvement of some Islamic banks to support Islamic crowdfunding. For example, Alliance Islamic Bank n Malaysia launched a crowdfunding platform, called SocioBiz, with social goals. The platform aims at creating socio-economic impact for individuals and small businesses who need funds or technical support for their micro projects. Interestingly, Alliance Islamic Bank and few other Islamic banks in Malaysia are also supporting another Islamic social financing platform run by Ethis Group and its foundation, Global Sadaqah. Through the platform, donations are raised for specific social causes in which the bank contributes with equivalent amount of each dollar donated by individuals, creating incentive for more donations.

All these examples confirm the possibility of crowdfunding to achieve the various social goals, not only because it provides capital access to social projects, but also because it provides low-income people with a good investment opportunity.

- allets

Electronic payment systems emerged decades ago and are still in continuous development. These include: electronic payment cards, online banking transfers, and e-money whereby money is transferred from one party to another in a matter of seconds. Since the beginning, charitable organizations and microfinance institutions benefited from these technological advancements in their social impact programmes where the electronic payments reduced operational cost and hence positively contributed to the societies. There is growing evidence that mobile payments and e-wallets have contributed significantly to reducing poverty rates in developing countries that have encouraged their spread.

The famous M-Pesa in Kenya as a good example. It started as simple mobile phone-based money transfer in 2007, turning today to a digital bank allowing users to deposit, withdraw, transfer money and get microfinancing services. Vodacom, a founder of M-Pesa, in partnership with Amana Bank, launched in the mid of 2019, a new service called Halal Pesa. Halal Pesa is a financial service intended to empower M-Pesa customers to deposit savings for hajj and make zakat contributions. Shari’a-compliant microfinance services are in the pipeline. Nevertheless, despite the issue of high compounding interest rates associated with some lending services, the spread of such digital payments, especially those made by mobile phones, are found to have a significant positive impact on the society. It had lifted at least 194,000 Kenyans out of extreme poverty and enabled 185,000 women to move from primary agriculture to selling (Suri & Jack, 2016). The positive social impact of such digital payments is not limited to the financial inclusion of poor in remote areas only but also the reduction of crime rate in other largely cash-based societies.

While mobile network-based money transfer using airtime succeeded in offering interesting solutions in some countries, the past two years have witnessed an unprecedented increase of number of internet-based e-wallets offered around the world. e-wallets are applications that enable the individuals to pay using their mobile phones by simply scanning a QR Code. Statistics indicate that by 2019 the number of users of this technology increased over 30 percent since 2017, reaching nearly 2.1 billion consumers around the world (The Business Times, 2019). This is expected to have a significant positive impact on business and start-ups since QR code payments facilitated by e-wallets can drive additional consumer traffic for small businesses and the new entrepreneurial venture. In fact, it is confirmed that e-wallets can particularly trigger a significant increase in small transactions for small merchants. Furthermore, new entrepreneurs who have just started their businesses can benefit a lot from the low costs and convenience offered by e-wallets. As such, e-wallets offerings have significant social impact especially for economies that need to support the growth of small and micro enterprises to fight poverty and reduce income inequality.

The social impact of e-wallet can also be seen from a financial inclusion perspective. This is because opening an e-wallet does not require going to any bank, rather than scanning few documents and few clicks on the mobile phone without incurring any costs. The requirements to open an account are much simpler as compared to opening an account at a bank, and document screening process is almost automated. Small merchants, such as street sellers, can use e-wallet services to receive money with lower commissions than the fees imposed by banks and giant credit and debit card providers, such as VISA and Mastercard. There are even some e-wallets that provide their payment services free to street sellers, according to a recent study conducted by the International Academy for Shari’ah Research in Islamic Finance (ISRA).

Though there are very few explicitly Shari’a-compliant e-wallets, many of the mainstream are deemed to fulfil Shari’a requirements anyway. If an e-wallet is card-based, then the Shari’a ruling will follow the ruling of the cards used. This is because a card-based e-wallet is simply providing another way to connect the card to the payment network. The flow of funds is exactly the same as someone tabbing their card into a POS device. If an e-wallet involves an e-money issuer who receives money from users in return to the e-money, then a Shari’a analysis of the operations and flow of funds is required to examine its compliance.

THOUGH THERE ARE VERY FEW EXPLICITLY SHARI’A-COMPLIANT E-WALLETS, MANY OF THE MAINSTREAM ARE DEEMED TO FULFIL SHARI’A REQUIREMENTS ANYWAY

In a nutshell, the relationship between the user and e-money issuer could be wakala (agency) in which the user appoints the e-money issuer as an agent to facilitate the transfer of payments to the merchants upon proceeding with any payment. This wakala contract between the user and e-money issuer is also accompanied with money paid in advance by the user to the e-money issuer upon reloading (top-up). Similar to Islamic banks in dealing with current account deposits, e-money issuers may use these funds. Of course, they must guarantee the value in that instance. Accordingly, similar to the current accounts in Islamic banks, the money advanced upon reloading (top-up) could be considered qard al-hassan (interest-free loan) as well. The key Shari’a issue would be on rewards. Rewards given by e-money issuers to users, if any, shall not be attached to the balance or duration of the money deposited in the e-wallets otherwise such reward could be deemed as riba (interest). Rewards attached to the usages of e-money (i.e., purchases) might be allowed on the basis that they are not related to the creditor-debtor relationship between users and e-money issuer. Such rewards are very similar to the discounts given by banks upon using their debit cards in specific stores or for specific products. Surely, e-money issuers might be required to follow other conditions to ensure end-to-end Shari’a compliance including managing the funds received from users in compliance with Shari’a.

Blockchain

Blockchain is a distributed ledger technology that has attracted a lot of attention in the last five years. The importance of this technology comes from the fact that it is the first technology that allows transforming distributed systems from a pure theory to a practical system. Using blockchain, users could have a full copy of the data. It further allows the users to store and exchange data directly between them without the need for a central server, which means eliminating the need for a central authority to process the data registration and entrust maintaining the data integrity. The idea of having a distributed system is not new, but it was not applicable within the traditional technology due to technical challenges related to data synchronization and reaching compatibility among users to implement any changes, in addition to other challenges related to protecting the integrity and confidentiality of data.

Although the first application of the blockchain ten years ago was the invention of the cryptocurrency, the latter is only one application of the wide range of potential applications.

In fact, blockchain already proved itself in various fields including social finance in the last two years. While jurisprudential views abound on the legitimacy of digital currencies, scholars agree that Shari’a law is not opposed to the blockchain technology itself. Blockchain is just a neutral technical tool that can be used legitimately or not. It is the application which could be Shari’a-compliant or not, depending on the structure, scope and result of application.

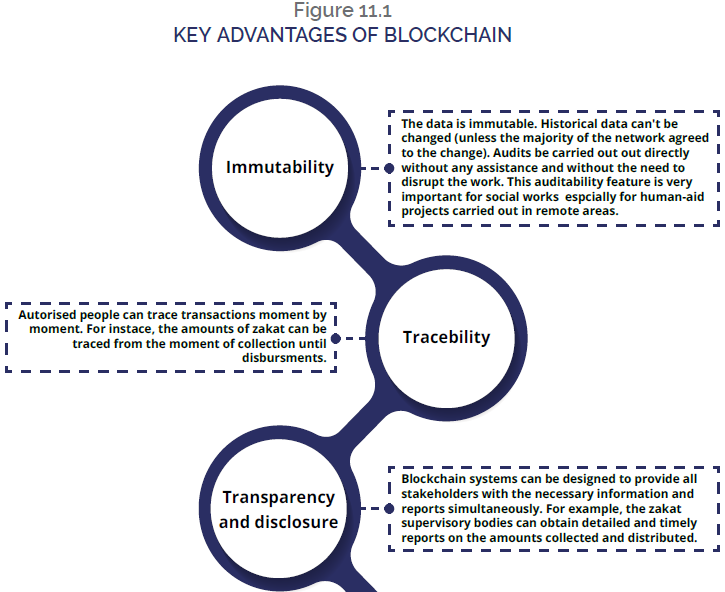

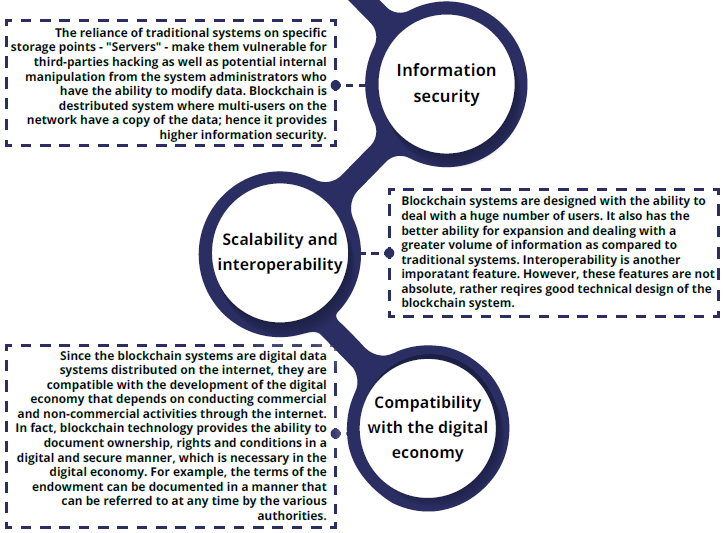

Among the most important advantages of using blockchain are the immutability, traceability and transparency of the data. Being a distributed system, blockchain facilitates the P2P transactions and increases efficiency. Scalability and compatibility with the digital economy are other key features of this technological advancement (see Figure 11.1). These features make blockchain a revolutionary technology that can be used in various fields including social finance. Reports often raised the governance as a main hinder of social programmes and related institutions. High administrative costs and lack of transparency are also often cited for charities and microfinancing. Accordingly, innovative projects to use blockchain in the social field started to emerge almost right after the spread of cryptocurrencies. However, the number of projects has increased substantially over the past three years. Hundreds of products and initiatives are launched. While some of these initiatives use cryptocurrencies in their design, others benefit from blockchain technology without using any of cryptocurrencies. Among these hundreds of projects, few are Islamic. However, there is a great potential for much more.

Different institutions have tried to apply blockchain differently. Consequently, today there is a wide range of products covering many social areas. The following subsections highlight some of these areas and present few examples that could help the reader to build an understanding around the current developments, and to appreciate the great potential of blockchain combined with other technologies in unlocking the future of IsSF.

Human Aid and Charity Led by the attractiveness of the blockchain features, especially its immutability and traceability, several projects have emerged to support philanthropy work through this technology. Founded in 2013, just a couple of years after the emergence of Bitcoin, BitGive is the probably the first non-profit organisation that is legally allowed to accept donations in Bitcoin. Earning a tax exemption status at the federal level in the United States, BitGive Foundation introduced GiveTrack platform that facilitates crowdfunding of philanthropy projects. Using Bitcoin, the platform provides the donors to track their donations until they reach their intended destination. Today, BitGive is certainly not the only blockchain-based philanthropy platform. Sikka, for instance, offers an innovative way to support individuals in Nepal in the event of disasters or calamities. Instead of using bitcoin, the platform gives the NGOs the ability to distribute Sikka tokens to the beneficiaries using a blockchain ecosystem created for this purpose. Beneficiaries can then exchange Sikka token for cash or goods from local vendors that are preregistered on Sikka platform. The key idea here is that this exchange and transfer of funds takes only seconds. Furthermore, even illiterate beneficiaries can use this advanced and innovative solution as Sikka tokens could be distributed in the form of a simple SMS. Yet, thanks to blockchain, NGOs are able to trace the efficiency of the operation and at the same time can ensure the timely distribution of their donations. In this way, donors can overcome the difficulties in delivering cash assistance as a result of poor infrastructure and other logistical constraints. Also, they can monitor the arrival of aid to their actual recipients beside following accounting and logistical arrangements.

Zakat

Zakat collections and distributions are often facilitated by specialized institutions. However, zakat institutions are often faced with challenges such as high operational costs. These costs are mainly related to the cost of the required governance structure. Corruption and mismanagement are also whispered as key sources of such high costs. Blockchain with its traceability feature probably provides one of the most promising solutions that could help in this regard. In fact, there are already few running in this field.

Blossom Finance, for instance, offered a service to pay zakat and sadaqa (alms) through bitcoin to facilitate the transfer of zakat funds from the rich countries to the poorer ones. The solution enables the zakat funds collected from any person or entity in the world to orphans and widows in the Sumatra and Central Java region of Indonesia through the company’s network of several charitable and non-profit organizations. The company receives zakat paid in bitcoin in the company’s cryptocurrency portfolio, then converts the bitcoins to the Indonesian rupiah and deposits the amounts in the accounts of the preregistered legal charities located in rural and poor areas in Indonesia. The company has obtained approval from its Shari’a Board to deduct the fees for converting bitcoin into rupiah from the zakat funds.

Although the above-mentioned structure does not enable much tracing and control over the funds, as it is built upon just a simple use of cryptocurrency as an intermediary, the solution benefits from the relatively cheaper and faster transfer for bitcoin as compared with traditional money transfer methods. However, the fluctuations of the exchange price of bitcoin and cryptocurrencies in general bring a lot of risks to such structure.

The International Academy for Shari’ah Research in Islamic Finance (ISRA) and Syscode have also developed a blockchain platform to support zakat distribution. The platform, which carry the name of ZakatTech, allows zakat payments to be recorded on federated blockchain database that enables tracing the donated funds at an unprecedented level. It provides easy and timely access to the information from time of collection to the time of distribution. The platform offers its services to zakat institutions and any other interested parties. The platform is also flexible in which the subscribing institutions can choose the appropriate levels of disclosure in accordance with their rules and regulations. Subscribing institutions can maintain the privacy and confidentiality of personal information by opting to encrypt sensitive information such as the identities of the benefactors. However, the system is able to generate aggregate reports based on their profiles. The system also allows identifying specific supervisory entities to verify operations before registration and audit transactions later in an easy and transparent manner without disturbing the workflow. The platform is distinguished from other solutions by high level of interoperability through offering blockchain as an infrastructure system that provides an opportunity for institutions that want to maintain their current systems and at the same time benefit from blockchain technology. For example, such institutions will be able to provide donors with the ability to track their donations and know how to use them and when to distribute them. The platform is ready in private sandbox environment and project leaders are looking to have the first pilot project with few institutions.

Waqf

Another important area that may benefit from blockchain technology is the Islamic endowment (waqf). ‘Smart contract’ features enabled by blockchain technology could be very helpful in this aspect. Smart contracts are simply self-executing contracts. The success factor behind smart contract is the convergence of the terms and conditions of the contract into codes. This will enable the automatic verification process in which, if the conditions are met, the contract is immediately concluded.

Few institutions have already tried to explore this in the last two years. Finterra Waqf Chain is one such example. It aims to tackle the challenges facing waqf by providing a crowdfunding platform that operates on blockchain. Despite the limited number of projects listed on the platform to date, the company hopes to attract waqf boards and interested stakeholders from around the world to submit their project plans. The Islamic Research and Training Institute of the Islamic Development Bank Group issued a press statement on October 17, 2019, announcing the establishment of a platform for the endowment as well, and it was called “Ishhad”. The said platform aims at documenting the endowments using FinTech, including the blockchain technology. There are no details available yet about the design of the platform, but it is hoped to provide endowment institutions and those around the world with the opportunity to benefit from the platform to achieve more transparency, protection and oversight. The ISRA, partnering with Syscode, is also looking into expanding their ZakatTech blockchain project to cover waqf as well.

Obviously, such solutions could reduce transaction costs and enable a greater level of efficiency of the distribution process while reducing system error and fraud rates. This ultimately will increase public confidence and increase waqf funds and proceeds of zakat and alms that are distributed to the most deserved people. Looking to this from macro perspective, an accurate aggregated data could be collected, and a lot of double work will be saved thanks to the ‘one point of truth’ created by blockchain data. Yet as of today, most of blockchain projects in the domain of zakat and waqf are still in their infancy stage. It will be too early to assess their actual performance, especially that most of them didn’t reach the economy of scale yet.

Microfinance

A World bank’s report indicates that there are about 1.7 billion people who do not have any bank account (World Bank, 2017). This, according to the United Nations, is an obstacle to obtaining their cash payments and financial services, and a barrier to those who wish to help them. Microfinance is probably the core traditional area of social finance that is hoped to help the unbanked poor people whether by providing small consumption loans or funding micro projects. With the emerging of electronic payment services mentioned before, some FinTech start-ups have tried to utilize blockchain technology to provide better data authentication and higher transparency of operations.

Looking to Islamic FinTech, there are already few projects trying to facilitate deposits and offer Shari’a-compliant microfinance services. Using blockchain, these projects aims to provide more transparency and higher governance that can encourage those who have surplus unds to contribute to the micro-projects. For instance, Blossom Finance has established an investment fund to finance small projects in Indonesia in cooperation with licensed microfinance institutions in Indonesia. The fund accepts contributions from around the world in dollars and in digital currencies such as Bitcoin and Ethereum in an effort to reduce the costs of remittances. The importance of such projects comes from the fact that it provides socially responsible investment opportunity to small investors from around the world. This enables middle- and low-income Muslims to help the poor. At the same time, they can obtain acceptable financial returns, thanks to the profit-sharing contracts established through the platform. The same company, Blossom Finance, has helped the Indonesian Islamic Microfinance Foundation (BMT) Bina Umma to raise financing in excess of US$50,000 through the issuance of “smart sukuk”, which is issued through smart contracts on the Blossom blockchain network.

The idea of smart sukuk has started to attract higher attention. This is because the issuance of traditional sukuk is highly costly due to the legal complexity and involvements of too many parties. Using blockchain technology, predesigned sukuk structure and contracts could be set as smart contracts allowing different parties to interact with higher trust and less need for legal scrutiny. As such, the traditional obstacles facing social impact investment could be removed by reducing costs of issuance and hence allowing the issuance of sukuk to finance small projects.

While the above examples benefit from blockchain by providing a wholesome solution to facilitate microfinance operations, other projects tried to tackle specific challenges facing microfinance, such as creating digital identity. Microfinance is often challenged by the high cost of reaching the poor unbanked populations and their limited official identification. Microfinance instructions customers are usually the ones having none or very limited official identification. They have limited ability to provide tangible security and often don’t have any credit history. This makes it extremely difficult for institutions to offer them any banking services. As mentioned before, mobile payments and e-wallets have helped in facilitating the work and reducing the operational cost but yet the issue of KYC is a pressing challenge that is hoped to be addressed using blockchain and other forms of FinTech. This is not purely theory, but there are already few pilot projects working in this respect. For instance, BanQu is working to create digital IDs for the poorest individuals by urging charities, companies and governments that deal with the poor on a daily basis to register their operations on a non-cryptocurrency blockchain platform designated for that. This company aims to create a database that helps the poor accessing financial services by providing financial institutions with the necessary information about them. The same applies to Bloom, which is trying to carry out assessments and credit ratings of financially marginalized groups, and to help financial institutions grant these groups credit facilities that would not have been granted in the absence of this information. Several other projects also tried to create IDs for refugees and to document the rights and ownerships of the marginalized groups such as the small farmers in remote areas of developing countries.

Agriculture Support and Halal Food Supply Chain

In addition to the above-mentioned social sectors, preserving the environment is one of the most important social responsibilities of all members of society. Providing healthy food for everyone is on the top priorities of UN and governments agendas. Given the ability of blockchain technology in providing a secure and transparent record of information, some applications have appeared to enhance the transparency of the food supply process through the registration of various information and events on the blockchain platforms from the moment the seeds are planted to the moment the final product reaches the consumer, including any manufacturing process in between. This will insure that agricultural products are clean, healthy and authentic. Similarly, this secure record can be very beneficial in insuring that the products contain no prohibited ingredients and the whole process is halal. Furthermore, such registration not only provides a secure recording of information over the authenticity of the product, but also eliminates unnecessary intermediaries and provides better access to agricultural markets. In practical terms, such applications can help small farmers expand their market where they can display and sell their products directly through the use of smart contracts technology. Through this technique, the farmer inserts the terms and conditions of sale and delivery so that it is presented to the merchant audience through the site or the programme for the system, and once the merchant accepts the terms, the contract is concluded and the necessary amount is transferred from the merchant account to a will of the trustee’s account to be transferred to the farmer in accordance with the terms and conditions. Approved later, at the same time the product ownership is transferred to the merchant and this is installed on the blockchain platform. All of this is done automatically according to the conditions agreed upon by the various parties without any interference from anyone, which gives more confidence to all parties.

GrainChain is one of the conventional examples that has existed already for few years. The company developed an online system that allows factories, farmers, merchants and drivers to communicate directly and conclude contracts without the need for intermediaries. Through this system, all concerned users can be sure about the specifications of the seeds, for example, and track the movement and conditions of storage from start to finish. Such information is supposed to be highly reliable, thanks to the non-adjustable blockchain database. Up to December 2019, GrainChain reported almost 2.6 million tons of agricultural products to be facilitated through the system. This amount is considered a large volume considering the novelty of this technology. However, while there are more than 20 similar conventional projects already in existence, we have yet to see successful projects leveraging on blockchain to ensure halal process. Nevertheless, few initiates are announced in 2019 by several FinTech developers.

Conclusion

Through the presented examples, it is evident that FinTech may bring a lot of benefits to IsSF. Equity crowdfunding, e-wallets and blockchain are three key areas of FinTech that have huge potentials for IsSF. While there are already many projects in the conventional arena, few Islamic initiatives are emerging. Although further Shari’a scrutiny of many project would require a comprehensive study of the structures and contracts used, many conventional social projects seem to be consistent with Shari’a requirements. Shari’a does not object to technology, it rather embraces the development which can help in preserving Muslims’ wealth and achieving HOS. New technologies can provide better governance and ensure higher efficiency. It can also help IsSF institutions in addressing specific challenges related to Shari’a compliance. Blockchain, in particular, seems to have high potential in bringing zakat and waqf to a next level. It can also provide interesting Islamic microfinance solutions, especially when combined with crowdfunding and advanced e-payment solutions. It can also bring credibility and trust to halal businesses.

{kind=link}