A global observer of takaful could easily be puzzled by the differences in its practice and implementation among countries. Why, for example, is the takaful model used in Egypt different from that used in Malaysia? One might also be perplexed as to why insurance is Shari’a-compliant in Iran but not in many other Muslim-majority countries. From this observation, a misconception might arise that there is no common understanding of takaful.

A practising Muslim’s obligations extend to how they live their life and earn their living. As an example, a Muslim is forbidden to earn interest. The ‘no return, without risk’ basic principle in Shari’a-compliant commercial transactions is the reason why earning interest is forbidden in Islam, as when interest is payable the lender reaps a return without taking any entrepreneurial risk. Indeed, in the Shar ’a vocabulary, the use of the word ‘loan’ only applies to benevolent loans, a loan made with no expectation to be repaid other than the amount extended, or indeed to be repaid at all.

The insurance contract has in it elements that are not consistent with a Muslim’s belief. Takaful is thus seen as meeting a need within this community. Another common assumption is that takaful is only for Muslims. This, perhaps, can be explained by the use of the Arabic word ‘takaful’, or ‘Shari’a insurance’ or ‘halal insurance’ to describe it. The reality is that takaful is just ‘doing insurance in a particular way’; you need not be a Muslim to subscribe to it. For a non-Muslim, takaful is another insurance product, while to a Muslim it is about ensuring fairness and transparency in the insurance contract.

VARIATION BETWEEN NATIONS

Yet another popular misconception is that takaful is a charitable institution. It is not and it cannot be in the regulated world that is insurance. Therein lies one of the reasons that the practice of takaful varies by country. The practical implementation of takaful is very much influenced by what the regulations in the country allow or do not allow. The takaful products available in a country are also determined by how solvency is determined. They require capital support. Policyholders do not provide working/solvency capital, but shareholders do, and so takaful products offered will depend on how much profit shareholders expect to reap for each unit of capital employed.

Capital in takaful is used to finance the ‘loan’ that the risk pool periodically requires either to fund a new business strain or bad claims experience. Capital is also required to finance risk capital for any mismatch between the liability profile and the assets backing this liability. All these considerations affect how the basic model is adjusted to meet shareholders’ expectations. The other reason takaful can vary between nations is the flexibility within which fiqh (Shari’a law) is implemented in different countries.

The Shari’a scholars in Iran, for example, examined the insurance contract and are able to explain away the elements which other Shari’a scholars in other countries deemed inconsistent with how business should be conducted to be consistent with fiqh muamalat (Shari’a law governing commercial transactions). The level of Shari’a compliance that is acceptable in any one country may also vary. Shari’a-compliant is different from Shari’a-based. The former has greater leeway in interpretation, while the latter leaves little room for variability. Generally, Shari’a compliance – where a Shari’a scholar or group of scholars give their blessings on a particular issue – is sufficient for acceptability among Muslims.

The basic commercial takaful model requires a separation between the shareholders’ capital and the policyholders’ fund (risk pool). Under this model, the takaful company informs the policyholder what percentage of the premium it is taking for its expenses and profit. The expense risk therefore rests with the shareholders. The remainder of the premium goes into the risk pool and is used to meet claims. The underwriting risk in this pool is thus shared among policyholders within the pool with any surplus being repaid as dividends to the policyholders.

Reinsurance is replaced with ‘retakaful’ and any net deficit is met through ‘loans’ financed by the shareholders’ fund. These loans are a first charge on the future surpluses from the risk pool. Thus, the risk-sharing element among policyholders in takaful extends through generations of policyholders. Transparency is addressed through the ‘fee’ payable from the premium at the point of entry into the pool and fairness through the sharing of surplus within the risk pool among the policyholders in that year. That is the theoretical basic takaful model – before factoring in the regulatory and Shari’a consequences mentioned before. The takaful company would have in its set-up a Shari’a advisory committee (SAC). This forms another layer of governance below the board of directors. The responsibility is to advise the board whether the takaful company’s operation is Shari’a-compliant. This compliance extends to the whole operating model (including sales, underwriting and investments), not just the takaful technical model.

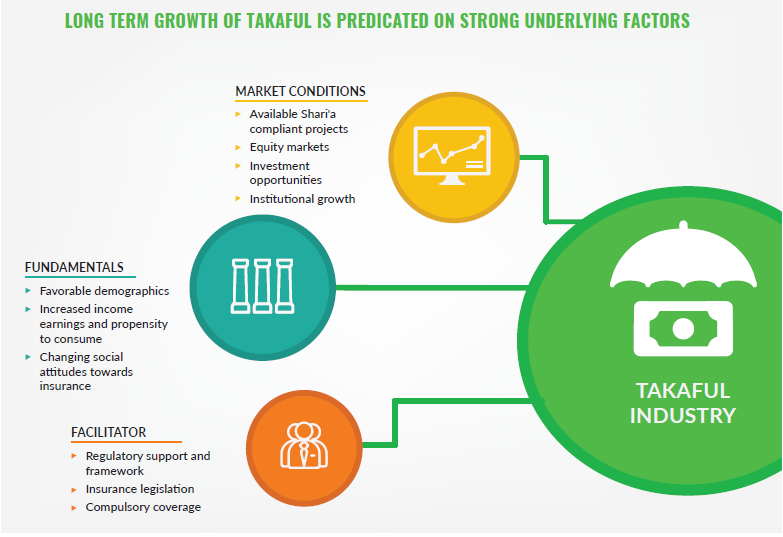

REASONS FOR GROWTH

The growth of takaful has been impressive, but this is primarily because the starting base is small. Takaful is more successful in countries where insurance generally has been successful. There are several reasons for this:

- The penetration for takaful corresponds with level of financial awareness among the population in the country. Also compulsory insurance (for example, motor) would similarly drive the demand for takaful.

- The main basis of distribution for takaful would be agents. Other than for compulsory products, takaful is ‘sold’ not bought. Thus in countries where insurance is sold through agents, we see greater success for takaful. As it needs to be explained to the consumer, this is another reason why agency is more successful than bancatakaful.

- Takaful companies are often newly set-up operations, requiring skilled human resources. A market with a thriving insurance industry can be a source of these skilled labours.

Policyholders do not provide working/solvency capital, but shareholders do, and so takaful products offered will depend on how much profit shareholders expect to reap for each unit of capital employed.

WHAT HAVE BEEN THE CHALLENGES FOR TAKAFUL?

After the initial period of euphoria about the potential of performance of the local stock market. Over the takaful globally, the industry has come to realise the formidable long term, the sustainability of takaful companies is challenges it faces to make a profit. These include: dependent on access to a sukuk market.

- Consumer expectations. Notwithstanding the significant

- The influence of regulations on the ability of Muslim market globally, takaful companies have come to takaful companies to make a profit cannot be realised that policyholders are the same whether it is takaful over emphasised. Stringent regulations require or insurance – they want the ‘cheapest’ offering. Thus, greater investments in systems and manpower. takaful companies compete on price with each other and The cost of regulations weighs more heavily for insurance companies. This is the slippery slope to ruin. new start-ups than for well-established insurance This is the slippery slope to ruin.

- Takaful companies are start-ups with limited capital, so companies. These costs make takaful operators less competing on price simply uses up capital without growing able to compete with the insurance industry. a loyal group of policyholders. It is also a fruitless exercise.

Is the takaful industry then doomed to slower growth Insurance companies do not have to share any underwriting going forward? Maybe. If takaful chooses to compete surplus with policyholders, and thus can recover faster in on price, it is unlikely to be a sustainable business model. any subsequent upturn in the insurance cycle.

- An undeveloped Islamic capital market. Takaful premiums request regulatory concessions. It is perhaps unrealistic to need to be invested, as premiums are paid before claims ask the regulator for concessions if its products are clones of are paid. Takaful is also a means to a disciplined approach insurance products.

• In many countries, takaful companies invest their policyholders’ and shareholders’ funds in the equity market. In such instances, the profitability of the takaful company is strongly correlated to the performance of the local stock market. Over the long term, the sustainability of takaful companies is dependent on access to a sukuk market.

• The influence of regulations on the ability of takaful companies to make a profit cannot be overemphasised. Stringent regulations require greater investments in systems and manpower. The cost of regulations weighs more heavily for new start-ups than for well-established insurance companies. These costs make takaful operators less able to compete with the insurance industry. Is the takaful industry then doomed to slower growth going forward? Maybe. If takaful chooses to compete on price, it is unlikely to be a sustainable business model. To be successful, it has to reinvent its business model or request regulatory concessions. It is perhaps unrealistic to ask the regulator for concessions if its products are clones of insurance products.

IDEAL IMPLEMENTATION

It would be unfortunate if takaful fails because of widespread misunderstanding of what it is and how it should be implemented. There are essentially two takaful markets and these should be considered separately. First, there is the market where currently only the insurance industry is serving. This consists of customers who are relatively financially aware of the importance of insurance as a means of risk management. For this market, takaful can be a success and can compete with insurance, as evidenced in Malaysia. What takaful needs to do to continue to grow is to reassess its product line and distribution costs. Insurance is expensive because distribution cost is expensive. Takaful needs to demonstrate that it can improve consumer outcomes compared with insurance. It should stick to its basic principles of providing consumers transparency and fairness. The other takaful market has to do with financial inclusion. Compared with other groups, Muslims are disproportionately distributed in poor and underdeveloped markets, where the commercial takaful model cannot work. There needs to be a different takaful model to apply to this underserved segment of the world’s population, Muslim or otherwise.

Takaful needs to demonstrate that it can improve consumer outcomes compared with insurance. It should stick to its basic principles of providing consumers transparency and fairness.

{kind=link}