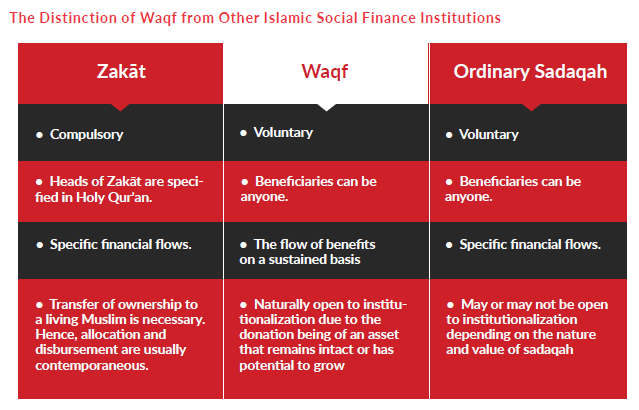

The institution of Waqf implies holding or setting aside certain physical assets by the donor (Waqif) and preserving it so that benefits continuously flow to a specified group of beneficiaries or community. A Cash Waqf is “the confinement of an amount of money by a founder(s) and the dedication of its usufruct in perpetuity to the welfare of society”. The nature of the expected benefit or purpose of the Waqf is clearly stated in the Waqf deed or document created for this purpose by the donor (Waqif). A traditional example of Waqf is that of donating or setting aside a land for construction of a masjid or a school or a hospital. The donor also specifies the trustee-manager(s) who would ensure that the intended benefits materialize and flow to the community. The trustee-manager is variously described as mutawalli or nazir.

Historically, in many Muslim societies, Waqf-based institutions were the sole providers (with no state intervention) of education, health care, water resources, and support for the poor. The list of social services even included the welfare of animals. The institution of Waqf by creating community assets has the potential to create robust sustainable entities that may address the education, healthcare and other social needs in Muslim societies. Thus, Waqf is a viable and sustainable funding option for socially beneficial projects, thereby reducing dependency on public funds.

GLOBAL OVERVIEW OF AWQĀF SECTOR

INDIA

There are more than 490,000 registered Awqaf spread over different states and union territories of In- dia. A large concentration of Waqf properties is found in West Bengal (148,200) followed by Uttar Pradesh (122,839). Other states with a sizeable number of Awqaf are Kerala, Karnataka and Andhra Pradesh. The total area under Waqf properties all over India is estimated at about 600,000 acres. As the book values of the Awqaf properties are about half a century old, the current value can safely be estimated to be several times more and the market value of the Waqf properties can be put at INR1.2 trillion (about US$20 billion).

BANGLADESH

In Bangladesh according to a survey conducted by the Bureau of Statistics of the Government of Bangladesh, the total number of Waqf properties in the country is 150,593 including 1,400 properties around different ‘mazars’.

According to the 1983 Mosque census, out of about 200,000 mosques 123,006 are Waqf properties. It is also claimed that almost one-third of the land of Dhaka city is Waqf. Out of the 150,593 Waqf properties, however, only 15,300 are registered with the Waqf Administration of the Government.

MALAYSIA

Data for Waqf by type of properties indicate that of the 6,406 pieces of Waqf properties; 1,760 pieces are for masjids, 900 pieces for suraus and 219 pieces for religious schools. A total of 2,446 pieces are for cemeteries, 15 pieces for house dwellings, 125 pieces for buildings, 314 pieces for paddy fields, 46 pieces for coconut planting, 42 pieces of rubber trees, and 8 pieces for gardening. Further, there are 38 pieces of orchards; 87 pieces of village lands, 37 pieces of empty lots, 367 pieces undefined and 2 pieces of strata title ownership. According to the Department of Awqaf, Zakat and Hajj (JAWHAR) of the government of Malaysia, the 11,091 hectares of land under Awqaf are valued at RM1.2 billion (the US$384 million). Nonetheless, the current statistics indicate that of Malaysia’s nearly 13 and a half thousand hectares of Waqf land, only two percent of the total area has actually been redeveloped. Awqaf hotels are the recent trend in the development of Waqf property. Four hotels have been built under the Waqf concept in the states of Malacca (Pantai Puteri), Perak (The Regency Seri Warisan), Terengganu (Grand Put-eri) and Negeri Sembilan (Klana Beach Resort).

INDONESIA

In Indonesia data obtained from the Ministry of Religious Affairs for the year 2012 indicate that the size of registered land Waqf in Indonesia is equal to 1,400 km² and most of them are still idle. The market value of registered land Waqf is estimated to be equal to Rp590 trillion (US$ 60 billion). Collected cash Waqf by Badan Wakaf is equal to Rp3.60 billion (US$370,000).

SINGAPORE

In Singapore as of 2012, the Waqf portfolio of MUIS includes 157 properties that comprise 114 shop-houses, 30 residential units, 10 commercial units, 2 commercial buildings and 1 institution. Size of land area under Waqf is 406,910 sq ft. The size of the net area that may be rented out is 447,233 sq ft. The portfolio is valued at S$471 million.

MAURITIUS

The country was among the early states to create a modern and dedicated law of Waqf, the Waqf Act 1941 under which it set up a Board of Waqf Commissioners to protect the community wealth and assets. As on date there are a total of 377 Waqfs comprising 105 family Waqfs, 150 religious Waqfs, and 122 philanthropic Waqfs. Waqf is grouped under Waqf-ul-lillah, the family Waqf is classified as the Waqf-ul aulad. The first Waqf registered under the Waqf Act dated 26th February 1942 and was a family Waqf (Waqf-ul aulad).

“THE INSTITUTION OF WAQF BY CREATING COMMUNITY ASSETS HAS THE POTENTIAL TO CREATE ROBUST SUSTAINABLE ENTITIES THAT MAY ADDRESS THE EDUCATION, HEALTHCARE AND OTHER SOCIAL NEEDS IN MUSLIM SOCIETIES.”

CONCLUSION AND POLICY RECOMMENDATIONS

In order for the institution of Waqf to play a meaningful role in solving development problems of contemporary Muslim societies, dynamism in laws and Waqf jurisprudence can help in revitalizing the institution of Waqf. Below are some policy recommendations to revive and revitalize the institution of Waqf.

POLICY RECOMMENDATIONS FOR THE GOVERNMENT

- To encourage the creation of Waqf other than in dormant real estate alone, private entities shall be incentivised to establish, manage and administer Waqf.

- To retain public confidence, the government shall not have the exclusive right to appropriate property unless through the court of law if there is usurpation or abuse by the trustees. Minimal intervention in the routine administration is necessary in order to encourage the private establishment of Waqf on the demand side and for financial institutions and corporations to offer wealth management services, especially in Cash Waqf on the supply side.

- It is important to provide tax incentives to engage more people and corporations towards establishing Waqf. Corporations that engage in corporate philanthropy can effectively establish corporate Waqf. The contributions to these Waqf by individual and corporate donors shall be made eligible for tax credit like it is the case with other recognized institutions.

- If a donor dedicates real estate to an existing Waqf or to establish a new Waqf, the taxes related to registration and transfer of property shall be exempted.

Waqf law should provide a comprehensive definition of Waqf that includes both permanent and temporary Waqf. It must also explicitly cover various types of Waqf: family and social Waqf, direct and investment Waqf, cash Waqf and corporate Waqf.

- There should be a balance between emphasis on preservation and development. To encourage private participation, there should be flexibility in the use of Waqf assets for investment in the form of leasing and financial investments. At the same time, it is important to have risk management guidelines to ensure the preservation of Waqf assets.

- Provisions should be added in the existing laws regarding ‘ibdal’ (exchange) and istibdal (substitution) of Waqf assets in order to revive the old Waqf assets, revitalize the existing ones and to ensure sustainable existence and utility of Waqf assets.

The legal framework should not restrict the definition of the endowed asset to immovable tangible assets only, such as, real estate, but should also explicitly recognize movable and financial assets, e.g. cash, stocks, gold, financial securities, transportation vehicles, books, computers, medical equipments, hospital beds etc.

- Laws must make it compulsory to have transparent and honest reporting of financials.

- Punitive actions shall be taken against the abuse or usurpation of assets by the trustees and in this regard, financial penalties should be complemented with physical punishments to act as strong deterrents.

POLICY RECOMMENDATIONS FOR ISLAMIC FINANCIAL INSTITUTIONS

- Islamic banks can facilitate the development of old Waqf assets by way of Diminishing Musharaka, Sale and Leaseback and Istisna in order to rebuild and renovate Waqf property for improved post-financing valuation as commercial buildings.

- Microenterprise Waqf can be established by Islamic banks to mobilize people’s social savings in the form of Cash Waqf donations and then disbursing these funds to the poor micro-entrepreneurs in the form of Qard- e-Hasan.

- Family Waqf shall also be recognized in the law and its administration services can be offered by financial institutions providing private wealth management services.

- Islamic banks like other banks collect donations for hospitals and educational institutions. Such institutions can mobilize funds through cash Waqf and the Islamic banks can become the collection, payment and investment agents. If a special tax credit is allowed to those who donate to cash Waqf through banks, it will help in financial inclusion and documenting the philanthropic third sector activities.

- The government can mobilise the funds through Cash Waqf for the shortfall in the annual federal development budget by engaging Islamic banks as the collecting agent to gain wide public participation and engagement.

- Waqf-based Islamic microfinance institutions can be established where the seed capital can be mobilized through cash Waqf. Islamic banks can use their existing resources, capacity and infrastructure to integrate financially excluded micro-borrowers into the financial system through this mechanism.

{kind=link}