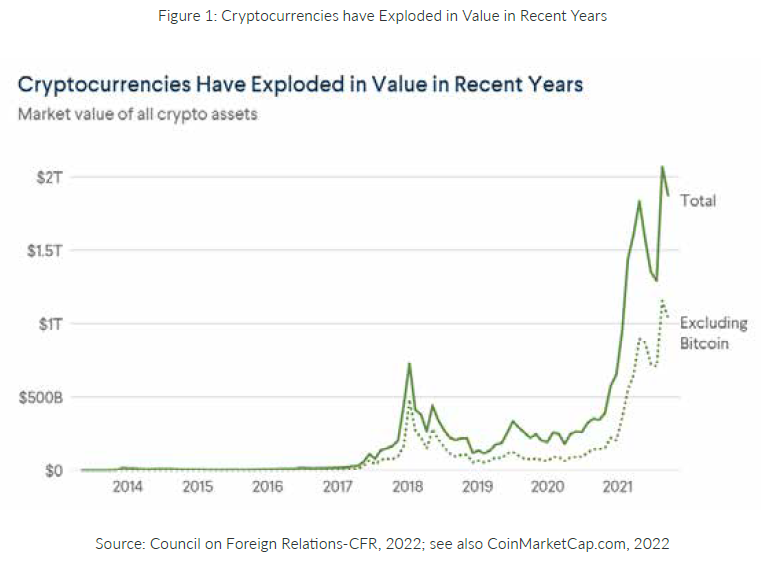

There is an adage that states “Nothing is more powerful than an idea whose time has come.” With the current ‘digitisation of civilisations’ – amplified further by the ongoing pandemic – cryptocurrencies have surged. They are one of the most discussed, unclear and controversial areas, perhaps because of their novelty or the effect of another adage “too much too soon”. Nevertheless, while still taken for granted as a ‘tech geek hobby’ the rise and impact of cryptos are enough to create a quiver beyond the geek groups.

So what’s the commotion? To know the dynamics and conclude a preliminary stance, it is important to understand the concept of crypto. What purpose, objective or problem statement does it help to solve and in doing so, does this innovation appear as ‘a smart boon or smart bane’? To address these questions, let’s start with the basic purpose it ought to serve.

The Main Purpose and Objective of Digital Cryptocurrencies

The pivotal purpose of cryptocurrency innovation is to resolve the issues marring the conventional currencies by resorting the power and responsibility in the hands of the end-user. Additionally, crypto must obey the normal properties of usual currency:

- fungible, 2) durable, 3) portable, 4) recognisable, and 5) stable while being a unit of account, store of value and standard of payment/deferred payment. The following are the common category classification of cryptos, Decentralised Finance- DeFi, Non-Fungible Tokens-NFT, Utility Tokens, Store of Value Tokens like Bitcoin and Litecoin, and Yield Farming tokens etc.

If it is a revolution that these cryptos ought to bring, then it is crucial to understand from a layman’s perspective what cryptos are.

Defining Crypto Currencies

These are some of the basic definitions of cryptocurrency given by different organisations and websites.

Oxford: “a digital currency in which transactions are verified and records maintained by a decentralised system using cryptography, rather than by a centralised authority”.

Trend Micro: “A cryptocurrency is an encrypted data string that denotes a unit of currency. It is monitored and organised by a peer-to-peer network called blockchain, which also serves as a secure ledger of transactions, e.g., buying, selling, and transferring.

… Bitcoin, Ether, Litecoin, and Monero are popular cryptocurrencies”.

Kaspersky: “Cryptocurrency is a digital payment system that doesn’t rely on banks to verify transactions. It’s a peer-to-peer system that can enable anyone anywhere to send and receive payments. When you transfer cryptocurrency funds, the transactions are recorded in a public ledger. Cryptocurrency is stored in digital wallets”.

Investopedia: “A cryptocurrency is a digital or virtual currency that is secured by cryptography, which makes it nearly impossible to counterfeit or double-spend”.

Webster: “any form of currency that only exists digitally, that usually hasno central issuing or regulating authority but instead uses a decentralised system to record transactions and manage the issuance of new units, and that relies on cryptography to prevent counterfeiting and fraudulent transactions.

Forbes: “A cryptocurrency is a medium of exchange that is digital, encrypted and decentralised. Unlike the U.S. Dollar or the Euro, there is no central authority that manages and maintains the value of a cryptocurrency. Instead, these tasks are broadly distributed among cryptocurrency’s users via the internet”.

At least one thing becomes clear from the above definitions; to clearly understand cryptocurrencies, one needs to first grasp the new age terminologies fully while also simultaneously becoming disconcerted by the aspects in these definitions e.g., no central or formal authority to create or manage, internet/ cyber reliance, risk of counterfeiting and frauds etc. If absorbing the theory of crypto is a complex, intensely interconnected, and upheaval learning effort, imagine the difficulty of adopting, launching, ex-ante and ex-post managing and sustaining the same. The ordeal becomes more plausible by looking at the commonly established pros and cons of such currency innovations.

Pros

- Cryptos have the potential to spur financial innovation

- Increase efficiencies through faster and cheaper payments

- Augment financial inclusion

- Anonymity

- Transparency

- Decentralisation

- Democratisation

- Potential for quick gain

CONS

- There is no real value

- There is no stabilising force

- Excessive cost and energy consumption to produce, raising further eyebrows in ESG and climate change

- Catalytic culture of speculation

- Unforeseen and amplified price, and market volatilities in scope and scale

- Unregulated and unbacked

- Issue of inheritance

- Unforeseen legal, tax and fiscal issues

- Conversely, concerns around safety, financial integrity (money laundering and evasion of capital controls)

- Last but not the least is the inevitable issue of cyber risk

There is a Conundrum!

Apart from the additional Shari’a and Islamic financial sector views, the facts this article has submitted till now present confusion, commotion and a presence of cognitive dissonance regarding crypto. The palpability of the crypto conundrum has surged so much that governments have taken stern choking measures. To control illicit activities, authorities have taken to delegate exchanges that deal in the conversion of cryptos to USDs and other respective currencies. Countries like China and Pakistan have put mining or dealing in or with cryptocurrencies under criminal offence. China, for instance, is among the world’s largest countries for Bitcoin mining, has officially banned all types of cryptocurrencies from September 2021, sending shock waves to the crypto world and a downward spiral. Mixed approaches followed suit sparring further ‘acceptability confusion’. Many other countries have followed the China, Pakistan trajectory while the rest are yet to take such a strict approach (see Figure 2).

Central Bank Digital Currencies-CBDCs

Despite all the voices, measures and sensations – for and against cryptos – one thing is for certain. In view of the rapid ‘digitalisation of civilisation’, there is no escaping digital currencies, hence only the shape could change before the formal inevitable acceptability. Nevertheless, as most game-changing innovations come, with or without serendipity, one such crypto-born digital novelty is the notion of ‘Central Bank Digital Currency’- CBDCs. The same signifies, not only the world succumbing to digital finance, but also aiming to preemptively or proactively assert sovereignty without undermining the speed, agility, smartness, and other advantages cryptos bring.

Reports (see atlanticcouncil.org) estimate that countries controlling more than 90% of the global economy are exploring CBDCs. China was quick to move in this direction by launching a digital Yuan in 2019/2020, currently estimated to be settling billions of dollars of commercial transactions. India has recently announced its ambitions for CBDCs.

Alongside the China phenomenon, the focus on CBDCs was further amplified by the ‘BigTechs’, when Google, Facebook and others come into the financial payments, digital currencies world via the launch of Lariba, Google and Samsung pay etc. The CBDCs versions of digital currency, with the added government/regulator control factor, may not only cover the loopholes of normal crypto but would essentially provide many smart tools for managing the economy, monetary policies, saving-investment behaviour and taming money supply backed via a ‘Digital Gold Bullion’ status; making CBDCs a safe, regulated, acceptable, smart and well-backed digital mass asset.

What’s for Economies Hosting Sectors Like Islamic Finance?

The question arises, what is in it for economies that mostly host Islamic finance as part of the financial sector? To me FinTech, BigTechs, TechFins and DeepTechs are nothing but a formal advent of what could be termed as “Digitisation or Atomisation of Civilisations”. However, it is plausible that the potentials could soon glide towards disconcertion if and only this smart financial amplification, currency or otherwise is not understood, absorbed and utilised via an ecosystem approach. Currently, the pandemic has ridden the global economy and which is already adjusting to navigate and adjust to a multipolar economic world that is grappling to mitigate ‘Black Swans’ while bracing for “Green Swans’ of Climate change.

Adopting technology orientations as mere fashion and not as an actual necessity could prove a misfire. The submission becomes more plausible via the assertion that the premier FinTech disruption models are nothing but a modern technology-oriented application of risk-sharing finance: the mandate of Islamic finance. Consequently, this builds the case for Islamic financial institutions to be more agile and receptive to adapting and adopting FinTech solutions.

With this as vision and ‘innovation, not renovation’ as mindset, a 2021 onward Version 2.0 of smart Islamic finance could be forecasted.

Understood and implemented as an ecosystem, Version 2.0 could be branded as a ‘New Age FinTech Islamic/Halal Finance. The ‘magic sauce’ for such an ecosystem would be to rely on an end-to-end understanding of innovation from renovation, FinTech from techfin, smart from anti-smart tech, constructive from anti-constructive innovation, enhancing social and financial inclusion innovation from anti the same. Only cognitive and synergy could lead to understanding, adoption and implementation as the most important prerequisite, making FinTech live up to its real promise, bearing new normal assets like big data, decentralisation, demonetisation and democratisation of financial services and operation.

A well-crafted approach to the above scheme shall necessarily allow for the most needed, useful, timely and well-acclimatised smart and sustainable Islamic finance, in line with local supply and demand of technology adoptions. The same subsequently shall make humans and societies actually and needfully smart, in line with the overall nature of an individual and the very society. Not doing so in a suited, phase-wise and submitted manner, runs the peril of running humankind against its nature, stimulating them as anti-social, anti-interactive and anti-smart i.e. not living up to their full potential, and boozed with over and perhaps unnecessary, untimely, forced reliance on technology.

This amplifies fertility for cyber risks and the dark side of technology for the end-user who is not end-to-end trained, internalised, well-timed and phase-wise glided to tech solutions of any sort, as per their own social, behavioural and cultural fabric. No wonder, for example, product innovation and new initiatives often hit the wall in such miss crafted environment.

Until now, Islamic/halal finance is usually constrained by end-to-end product innovation, however, with a digital/technological alternative, “that is necessarily not anti-human” would hold the key for not only fixing product creation issues but the overall progress of Islamic finance, meeting its actual mandate of end-to-end Maqasid Al Shari’a fulfilment with sustainability. A smart, automated and nature-dependent new normal model of Shari’a finance could be linked to

better and smartly serve the UN’s SDGs, VBI and the overall Halal economy. For example, a well-suited adoption of blockchain and mobile technology could help provide and promote Smart Islamic Banking Contracts (SIBCs) solution (adjustable to fine-tune with specificities of regions) and also smart data supply for customer risk profiling and investment risks.

Concluding a transparent contract to finance Shari’a-based deposits and products could then be a mobile app working with financial institutions smartly equipped to assess risks like the novel payment systems, along with SIBCs. These could be the basic attractive modes to ease international trade deals for Islamic industry (including takaful) as well as an increased customer base that is getting necessarily tech-savvy by the day. The value and mechanics of the same could be fully chiselled and endorsed/ accredited by WTO, World Bank, IFSB & AAOIFI.

Islamic Wealth & Asset Management could be served via marketplaces, driven by robo-advisory/AI and Numerie. This would also transform and lubricate sukuk for public-private partnerships, financings institutional investments, crowdfunding, angle investing, and P2P financings. Promoting the same as “New Age Techno Islamic finance”. A red alert in all this shall be how to re-orient and re-understand the new-age risks that are cyber in nature and black to green swans in effect and process. This shall make RegTech supervision/techvision that much more proactively important with activity rather than entity-based regulatory model augmenting the promise to either miss or hit a home-run via the new opportunities on offer.

{kind=link}